| 1 |

Executive Summary |

| 1.1 |

Major Findings & Conclusions |

| 1.2 |

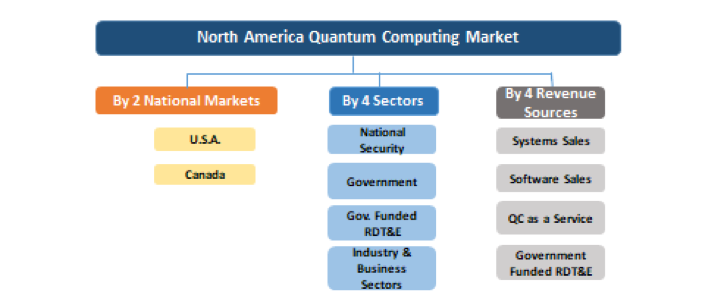

North America Quantum Computing Market – 2018-2024 |

| 1.2.1 |

North America Quantum Computing Market by Sector |

| 1.2.2 |

North America Quantum Computing Market by Revenue Source |

| |

|

| |

MARKET BACKGROUND & ANALYSIS |

| 2 |

Quantum Computing Market Background |

| 2.1 |

The Global Information Technology (IT) Market |

| 2.2 |

Quantum Computing |

| 2.3 |

Why Are Quantum Computers Attractive? |

| 2.4 |

Quantum Computing Outlook |

| 2.5 |

Quantum Supremacy |

| 2.6 |

Quantum Technologies Timeline |

| 2.7 |

Investments in Quantum Computing |

| 2.8 |

Quantum Computing Technology Roadmap |

| 2.9 |

Topological Quantum Computers |

| 2.1 |

The 2nd Quantum Revolution |

| 2.11 |

Applications of Quantum Computing |

| 2.12 |

The Private Sector Quantum Computing R&D Activities |

| 2.13 |

The Global Quantum Computing Race |

| 2.14 |

China – U.S. Quantum Information Leadership Race |

| 3 |

Quantum Information Bids, Tenders and Projects Data |

| 4 |

SWOT Analysis |

| 4.1 |

Strengths |

| 4.2 |

Weaknesses |

| 4.3 |

Opportunities |

| 4.4 |

Threats |

| 5 |

Quantum Computing Value Chain |

| 6 |

Quantum Computing Vertical Markets |

| 6.1 |

Defense & Intelligence Quantum Computing Market |

| 6.1.1 |

National Security Intelligence |

| 6.1.2 |

Defense |

| 6.2 |

Homeland Security & Public Safety Quantum Computing Market |

| 6.2.1 |

Public Safety |

| 6.2.2 |

Homeland Security |

| 6.3 |

Government & Public Services Quantum Computing Market |

| 6.4 |

Gov.-Funded RDT&E Quantum Computing Market |

| 6.5 |

Banking & Securities Quantum Computing Market |

| 6.6 |

Manufacturing & Logistics Quantum Computing Market |

| 6.7 |

Insurance Quantum Computing Market |

| 6.8 |

Healthcare & Pharmaceutical Quantum Computing Market |

| 6.8.1 |

Overview |

| 6.8.2 |

Medical Diagnostics Quantum Computing Market Background |

| 6.8.3 |

Medical Treatments Quantum Computing Market Background |

| 6.8.4 |

Example: Combating Cancer |

| 6.8.5 |

The Folding@home Project |

| 6.8.6 |

Pharmacology Quantum Computing |

| 6.8.7 |

Protein Folding Quantum Computing Market Background |

| 6.9 |

Retail & Wholesale Quantum Computing Market |

| 6.1 |

Information Technology Industry Quantum Computing Market |

| 6.11 |

Telecommunications Quantum Computing Market |

| 6.12 |

Automotive, Aerospace & Transportation Quantum Computing Market |

| 6.13 |

Energy & Utilities Quantum Computing Market |

| 6.14 |

Web, Media & Entertainment Quantum Computing Market |

| 6.15 |

Smart Cities Quantum Computing Market |

| 6.16 |

Cybersecurity Quantum Computing Market |

| |

|

| |

REGIONAL MARKET |

| 7 |

North America Quantum Computing Market – 2018-2024 |

| 7.1 |

North America Quantum Computing Market by Sector |

| 7.1.1 |

Market Forecast – 2016-2024 |

| 7.1.2 |

Market Dynamics – 2016-2024 |

| 7.1.3 |

Market Breakdown – 2016-2024 |

| 7.2 |

North America Quantum Computing Market by Revenue Source |

| 7.2.1 |

Market Forecast – 2016-2024 |

| 7.2.2 |

Market Dynamics – 2016-2024 |

| 7.2.3 |

Market Breakdown – 2016-2024 |

| |

|

| |

NATIONAL MARKETS |

| 8 |

U.S. Quantum Computing Market – 2018-2024 |

| 8.1 |

U.S. Market Background |

| 8.2 |

U.S. Quantum Computing Market Background |

| 8.2.1 |

U.S. Government Quantum Computing |

| 8.2.2 |

U.S. Government Investment in Quantum Computing: Introduction |

| 8.2.3 |

DOD: Quantum Computing Activities, Projects & Funding |

| 8.2.4 |

DOE: Quantum Computing Activities, Projects & Funding |

| 8.2.5 |

NSA: Quantum Computing Activities, Projects & Funding |

| 8.2.6 |

IARPA: Quantum Computing Activities, Projects & Funding |

| 8.2.7 |

NIST: Quantum Computing Activities, Projects & Funding |

| 8.2.8 |

NSF: Quantum Computing Activities, Projects & Funding |

| 8.2.9 |

U.S.A. Supercomputing Race |

| 8.2.10 |

Federal Quantum Computing Outlook – 2018-2024 |

| 8.2.11 |

U.S. Private Sector Quantum Computing Market Background |

| 8.2.12 |

U.S. Quantum Computing RDT&E |

| 8.3 |

The U.S.-Chinese, Quantum Technology Race |

| 8.3.1 |

Scope |

| 8.3.2 |

U.S. Strategic Considerations |

| 8.3.3 |

Quantum Encryption and Communication Race |

| 8.3.4 |

The Quantum Sensing Race |

| 8.4 |

U.S. Quantum Computing Market – 2016-2024 |

| 8.4.1 |

Market Forecast – 2016-2024 |

| 8.4.2 |

Market Dynamics – 2016-2024 |

| 9 |

Canada Quantum Computing Market – 2018-2024 |

| 9.1 |

Canada Market Background |

| 9.2 |

Canada Quantum Computing Market Background |

| 9.3 |

Canada Quantum Computing Market – 2016-2024 |

| 9.3.1 |

Market Forecast – 2016-2024 |

| 9.3.2 |

Market Dynamics – 2016-2024 |

| |

|

| |

COMPANIES & BUSINESS OPPORTUNITIES |

| 10 |

Business Opportunities |

| 10.1 |

Quantum Computing Business Opportunities Roadmap |

| 10.2 |

Machine Learning |

| 10.3 |

Search Engines |

| 10.4 |

Business Intelligence |

| 10.5 |

Software/Hardware Validation and Verification |

| 10.6 |

Image and Pattern Recognition |

| 10.7 |

National Security Intelligence |

| 10.8 |

Defense |

| 10.9 |

Public Safety |

| 10.1 |

Homeland Security |

| 10.11 |

Government & Public Services |

| 10.12 |

Banking & Financial Services |

| 10.13 |

Financial Electronic Trading & Trading Strategies |

| 10.14 |

Smart Manufacturing & Logistics |

| 10.15 |

Mission Planning/Scheduling and Logistics |

| 10.16 |

Insurance |

| 10.17 |

Medical Diagnostics |

| 10.18 |

Medical Treatments |

| 10.19 |

Pharmacology |

| 10.2 |

Protein Folding |

| 10.21 |

Retail & Wholesale |

| 10.22 |

Information Technology Industry |

| 10.23 |

Telecommunication |

| 10.24 |

Automotive & Transportation |

| 10.25 |

Aerospace |

| 10.26 |

Energy & Utilities |

| 10.27 |

Energy Systems & Photovoltaics |

| 10.28 |

Energy Exploration |

| 10.29 |

Web, Media & Entertainment |

| 10.3 |

Smart Cities |

| 10.31 |

Cybersecurity |

| 10.32 |

Quantum Computing Systems |

| 10.33 |

Quantum Computing Software |

| 10.34 |

Quantum Computing as a Service on the Cloud |

| 10.35 |

Academia & National Labs |

| 10.36 |

Graph Theory Problems |

| 10.37 |

Material Science |

| 10.38 |

Marine Science |

| 10.39 |

Bioinformatics |

| 10.4 |

Climate Modeling & Weather Predictions |

| 10.41 |

Seismic Survey |

| 10.42 |

Risk Management |

| 10.43 |

Simulation |

| 10.44 |

Video Compression |

| 10.45 |

Cryptography |

| 10.45.1 |

Quantum Cryptography |

| 10.45.2 |

Post-quantum Cryptography |

| 10.46 |

QC Based Optimization Problems |

| 10.46.1 |

Optimization Problems |

| 10.46.2 |

Quantum-Assisted Optimization |

| 10.46.3 |

Reservoir Optimization Applications |

| 10.46.4 |

Utilities Management Optimization |

| 10.47 |

Quantum Computing Based Machine Learning |

| 10.47.1 |

Quantum Machine Learning |

| 10.47.2 |

Quantum Reinforcement Learning |

| 10.48 |

Big Data & Predictive Analytics |

| 10.49 |

Material Science |

| 10.5 |

Quantum Sampling |

| 10.51 |

Quantum Chemistry |

| 10.52 |

Monte Carlo Simulation |

| 11 |

Moore’s Law Outlook |

| 12 |

Quantum Computing Startups |

| 13 |

Quantum Computing Companies |

| 13.1 |

1Qbit |

| 13.1.1 |

Company Profile |

| 13.1.2 |

Quantum Computing Activities |

| 13.2 |

Agilent Technologies |

| 13.2.1 |

Company Profile |

| 13.2.2 |

Quantum Computing Activities |

| 13.3 |

Aifotec AG |

| 13.3.1 |

Company Profile |

| 13.3.2 |

Quantum Computing Activities |

| 13.4 |

Airbus Group |

| 13.4.1 |

Company Profile |

| 13.4.2 |

Quantum Computing Activities |

| 13.5 |

Alcatel-Lucent |

| 13.5.1 |

Company Profile |

| 13.5.2 |

Quantum Computing Activities |

| 13.6 |

Alibaba Group Holding Limited |

| 13.6.1 |

Company Profile |

| 13.6.2 |

Quantum Computing Activities |

| 13.7 |

Anyon Systems, Inc |

| 13.7.1 |

Company Profile |

| 13.7.2 |

Quantum Computing Activities |

| 13.8 |

Artiste-qb.net |

| 13.8.1 |

Company Profile |

| 13.8.2 |

Quantum Computing Activities |

| 13.9 |

Avago Technologies |

| 13.1 |

Booz Allen Hamilton |

| 13.10.1 |

Company Profile |

| 13.10.2 |

Quantum Computing Activities |

| 13.11 |

British Telecommunications (BT) |

| 13.11.1 |

Company Profile |

| 13.11.2 |

Quantum Computing Activities |

| 13.12 |

Cambridge Quantum Computing Limited |

| 13.12.1 |

Company Profile |

| 13.12.2 |

Quantum Computing Activities |

| 13.13 |

Ciena Corporation |

| 13.13.1 |

Company Profile |

| 13.13.2 |

Quantum Computing Activities |

| 13.14 |

Cyoptics |

| 13.14.1 |

Company Profile |

| 13.14.2 |

Quantum Computing Activities |

| 13.15 |

D-Wave Systems Inc |

| 13.15.1 |

Company Overview |

| 13.15.2 |

Quantum Computing Activities |

| 13.16 |

Eagle Power Technologies, Inc |

| 13.16.1 |

Company Profile |

| 13.16.2 |

Quantum Computing Activities |

| 13.17 |

Emcore Corporation |

| 13.17.1 |

Company Profile |

| 13.17.2 |

Quantum Computing Activities |

| 13.18 |

Enablence Technologies |

| 13.18.1 |

Company Profile |

| 13.18.2 |

Quantum Computing Activities |

| 13.19 |

Entanglement Partners |

| 13.2 |

Fathom Computing |

| 13.20.1 |

Company Profile |

| 13.20.2 |

Quantum Computing Activities |

| 13.21 |

Finisar Corporation |

| 13.22 |

Fujitsu Limited |

| 13.22.1 |

Company Profile |

| 13.22.2 |

Quantum Computing Activities |

| 13.23 |

Google Quantum AI Lab |

| 13.23.1 |

Company Profile |

| 13.23.2 |

Quantum Computing Activities |

| 13.24 |

H-Bar Quantum Consultants |

| 13.25 |

Hewlett Packard Enterprise Company |

| 13.25.1 |

Company Profile |

| 13.25.2 |

Quantum Computing Activities |

| 13.26 |

IBM |

| 13.26.1 |

Company Profile |

| 13.26.2 |

Quantum Computing Activities |

| 13.27 |

ID Quantique |

| 13.27.1 |

Company Profile |

| 13.27.2 |

Quantum Computing Activities |

| 13.28 |

Infinera Corporation |

| 13.28.1 |

Company Profile |

| 13.28.2 |

Quantum Computing Activities |

| 13.29 |

Intel Corp. |

| 13.29.1 |

Company Profile |

| 13.29.2 |

Quantum Computing Activities |

| 13.3 |

IonQ |

| 13.30.1 |

Company Profile |

| 13.30.2 |

Quantum Computing Activities |

| 13.31 |

JDS Uniphase Corporation |

| 13.32 |

Kaiam Corporation |

| 13.32.1 |

Company Profile |

| 13.32.2 |

Quantum Computing Activities |

| 13.33 |

Lockheed Martin Corp. |

| 13.33.1 |

Company Profile |

| 13.33.2 |

Quantum Computing Activities |

| 13.34 |

MagiQ Technologies, Inc. |

| 13.34.1 |

Company Profile |

| 13.34.2 |

Quantum Computing Activities |

| 13.35 |

Microsoft Quantum Architectures and Computation Group (QuArC) |

| 13.35.1 |

Company Profile |

| 13.35.2 |

Quantum Computing Activities |

| 13.36 |

Mitsubishi Electric Corp. |

| 13.36.1 |

Company Profile |

| 13.36.2 |

Quantum Computing Activities |

| 13.37 |

NEC |

| 13.37.1 |

Company Profile |

| 13.37.2 |

Quantum Computing Activities |

| 13.38 |

Nokia Bell Labs |

| 13.38.1 |

Company Profile |

| 13.38.2 |

Quantum Computing Activities |

| 13.39 |

NTT Basic Research Laboratories & NTT Secure Platform Laboratories |

| 13.39.1 |

Company Profile |

| 13.39.2 |

Quantum Computing Activities |

| 13.4 |

Optalysys Ltd. |

| 13.40.1 |

Company Profile |

| 13.40.2 |

Quantum Computing Activities |

| 13.41 |

Post-Quantum |

| 13.41.1 |

Company Profile |

| 13.41.2 |

Quantum Computing Activities |

| 13.42 |

QbitLogic |

| 13.42.1 |

Company Profile |

| 13.42.2 |

Quantum Computing Activities |

| 13.43 |

QC Ware Corp. |

| 13.43.1 |

Company Profile |

| 13.43.2 |

Quantum Computing Activities |

| 13.44 |

Quantum Circuits |

| 13.44.1 |

Company Profile |

| 13.45 |

Quantum Hardware Inc |

| 13.45.1 |

Company Profile |

| 13.45.2 |

Quantum Computing Activities |

| 13.46 |

QuantumCTek |

| 13.46.1 |

Company Profile |

| 13.46.2 |

Quantum Computing Activities |

| 13.47 |

Qubitekk |

| 13.47.1 |

Company Profile |

| 13.47.2 |

Quantum Computing Activities |

| 13.48 |

Quintessence Labs |

| 13.48.1 |

Company Profile |

| 13.48.2 |

Quantum Computing Activities |

| 13.49 |

QxBranch |

| 13.5 |

Raytheon BBN |

| 13.50.1 |

Company Profile |

| 13.50.2 |

Quantum Computing Activities |

| 13.51 |

Rigetti Computing |

| 13.51.1 |

Company Profile |

| 13.51.2 |

Quantum Computing Activities |

| 13.52 |

SeQureNet |

| 13.53 |

SK Telecom |

| 13.53.1 |

Company Profile |

| 13.53.2 |

Quantum Computing Activities |

| 13.54 |

Sparrow Quantum |

| 13.54.1 |

Company Profile |

| 13.54.2 |

Quantum Computing Activities |

| 13.55 |

Toshiba |

| 13.55.1 |

Company Profile |

| 13.55.2 |

Quantum Computing Activities |

| 13.56 |

Xanadu |

| |

|

| |

APPENDICES |

| 14 |

Appendix A: Introduction to Quantum Computing |

| 14.1.1 |

Superposition |

| 14.1.2 |

Entanglement |

| 14.1.2.1 |

Ion-based Qubits |

| 14.1.2.2 |

Superconducting Qubits |

| 14.1.2.3 |

Solid-State Spin Qubits |

| 15 |

Appendix B: Quantum Information Technologies |

| 15.1 |

Quantum information |

| 15.2 |

Shared Principles |

| 15.3 |

Quantum Computing |

| 15.4 |

Quantum Cryptography: |

| 15.5 |

Quantum Sensing |

| 16 |

Appendix C: Quantum Computing Hardware |

| 17 |

Appendix D: Quantum Computing Software |

| 17.1 |

Introduction to Quantum Algorithms |

| 18 |

Appendix E: Quantum Encryption |

| 18.1 |

Background |

| 18.2 |

Key Findings |

| 18.3 |

Spooks Reacting at a Distance |

| 19 |

Appendix F: Global 50 Top Supercomputers |

| 20 |

Appendix G: Industry Investment in Quantum Computing – 2006-2016 |

| 21 |

Appendix H: NQIT R&D Projects |

| 21.1 |

Background |

| 21.2 |

Architectures, Standards and Systems Integration |

| 21.3 |

Ion Trap Node Engineering |

| 21.4 |

Atom-photon Interfaces |

| 21.5 |

Photonic Network Engineering |

| 21.6 |

Solid State Node Engineering |

| 21.7 |

Secure Communications and Verification |

| 21.8 |

Networked Quantum Sensors |

| 21.9 |

Quantum Digital Simulation |

| 21.1 |

Hybrid Classical/Quantum Computing |

| 21.11 |

Capabilities and Support |

| 22 |

Appendix I: Exascale Computing |

| 22.1 |

Exascale Computing Definition |

| 22.2 |

U.S. Exascale Computing Activities |

| 22.3 |

China Exascale Computing Activities |

| 22.4 |

EU Exascale Computing Activities |

| 22.5 |

Japan Exascale Computing Activities |

| 22.6 |

India Exascale Computing Activities |

| 22.7 |

Exascale Computing Challenges |

| 23 |

Appendix J: Market Background by Country |

| 23.1 |

U.S. Market Background |

| 23.1.1 |

Facts & Figures |

| 23.1.2 |

U.S. Economy |

| 23.1.3 |

Department of Homeland Security |

| 23.1.3.1 |

Department of Homeland Security: Agencies and Units |

| 23.1.4 |

Department of Defense (DOD) |

| 23.1.5 |

Department of Justice (DOJ) |

| 23.1.6 |

Federal Bureau of Investigation (FBI) |

| 23.1.7 |

Department of State (DOS) |

| 23.1.8 |

National Aeronautic & Space Administration (NASA) |

| 23.1.9 |

Department of Transportation (DOT) |

| 23.1.9.1 |

Department of Commerce (DOC) |

| 23.1.10 |

U.S. Police Forces |

| 23.2 |

Canada Market Background |

| 23.2.1 |

Facts & Figures |

| 23.2.2 |

Canada Geopolitical Overview |

| 23.2.3 |

Canada Economy |

| 23.2.4 |

Canada Defense, Intelligence, Law Enforcement & Homeland Security Agencies |

| 23.2.5 |

Canadian Police Forces |

| 23.2.6 |

Canada Intelligent Services |

| 23.2.7 |

Canada Defense Forces |

| 23.3 |

Mexico Market Background |

| 23.3.1 |

Facts & Figures |

| 23.3.2 |

Mexico Geopolitical Overview |

| 23.3.3 |

Mexico Economy |

| 23.3.4 |

Mexico Defense, Intelligence, Law Enforcement & Homeland Security Agencies |

| 23.3.5 |

Mexican Police Forces |

| 24 |

Appendix K: Key Quantum Computing Patents |

| 24.1 |

Patents List |

| 24.2 |

Quantum Computing Patent Filing by Country |

| 25 |

Appendix L: Links to 31 Quantum Computing Academic Research Centers |

| 26 |

Appendix M: 2017 Quantum Conferences Links – |

| 27 |

Appendix N: Glossary |

| 28 |

Appendix O: References |

| |

|

| 29 |

Scope & Methodology |

| 29.1 |

Research Scope |

| 29.2 |

Research Methodology |

| 30 |

Disclaimer & Copyright |